Grocery Update Volume 2, #15: Why Sprouts Is Winning. For Now.

Also: Gaza’s Starvation Is A Crime Against Humanity. And 45,000 Grocery Workers Ratify New Contracts.

Discontents: 1. 45,000 GROCERY WORKERS RATIFY NEW CONTRACTS. 2. Gaza’s Starvation Is A Crime Against Humanity. 3. Why Sprouts Is Winning. For Now.

1. 45,000 GROCERY WORKERS RATIFY NEW CONTRACTS.

Members of United Food and Commercial Workers (UFCW) Locals 135, 324, 770, 1167, 1428 and 1442 voted to ratify a new three-year contract with Ralphs, a subsidiary of Kroger, and Albertsons (Albertsons, Vons and Pavilions). The contracts were reached after months of negotiations and active participation from thousands of Southern California grocery workers.

The six UFCW Locals released the following statement:

“The journey to contract ratification saw a record turnout of grocery workers, customers, and community members, all fighting for the same thing – better stores, better lives, better communities. They fought to ensure that grocery workers could feed their own families and afford health benefits and a dignified retirement at the end of a long career. They also fought for more staffing to improve the customer experience at their stores.

“Their fight took to the streets where they organized numerous rallies and marches that showed their power. It took to their stores where they stood up and demonstrated their unity by signing petitions and wearing buttons. Grocery workers also joined with customers in the fight for better staffing, talking to over 3,000 customers about their shopping experiences and sharing their feedback with these companies that can afford to do better. These actions built the strength needed to reach this agreement. Only by rising up together were grocery workers able to make a change in their workplaces that will benefit all grocery workers and customers in the future.”

Key provisions of the agreement include:

Substantial wage increases

A new supplemental pension plan to help workers in their retirement

Increased healthcare benefit contributions and faster healthcare eligibility for new hires

Staffing language that includes the union in evaluating reasonable staffing levels that address efficient operation of the store, the health and safety of employees, and the quality of customer service

This contract will go into effect immediately for over 45,000 essential grocery workers in Ralphs, Albertsons, Vons and Pavilions locations across Southern California.

Workers at Stater Bros., Gelson’s, Super A, and El Super stores in Southern California are currently negotiating similar terms with their employers.

(Disclaimer: Perspectives do not reflect those of our sponsors.)

2. Gaza’s Starvation Is A Crime Against Humanity.

IPES-Food Statement on the Genocide In Gaza.

Mass starvation is deliberately being used by Israel as a tool of genocide against the Palestinian people. The intentional denial of food and water in Gaza is a crime against humanity, a violation of the international human right to food, and a breach of humanitarian law. IPES-Food fully condemns the actions being taken by Israel, and the governments and corporations around the world fueling the deliberate and systematic weaponization of food and water against the people of Palestine.

This “man-made mass starvation” is the latest assault in a decades-long campaign of dispossession and oppression, which has now been acknowledged by governments around the world, the International Court of Justice, and major Israeli human rights groups. In November 2024, the International Criminal Court issued arrest warrants for Israeli Prime Minister Benjamin Netanyahu and former defense minister Yoav Gallant citing allegations of war crimes and crimes against humanity, specifically for using starvation as a method of warfare. Earlier this year, this crisis was named “the largest and fastest starvation campaign in modern history” by the UN Special Rapporteur on the Right to Food.

Today, Gazans are facing the lowest level of food consumption since the conflict began, with more people dying of starvation in the past 2 weeks than the previous 21 months. The UN World Food Programme has estimated that at least 470,000 people are enduring famine-like conditions, with 90,000 women and children needing urgent nutrition treatment. Since April 2025, more than 20,000 children have been admitted for acute malnutrition, with many dying of starvation and lack of humanitarian assistance. These figures are likely severely underestimated, as full assessments have remained near impossible to conduct due to ongoing violence and obstruction of humanitarian access.

When food can be accessed at all, prices have skyrocketed, including an almost 3,000% increase in the cost of flour and a close to 5,000% increase in the price of staple fruits and vegetables between October 2023 and July 2025. At the same time, more than 97% of water from the Gaza Strip's main coastal aquifer no longer meets WHO water quality standards, leaving residents dependent on Israeli-owned pipelines for most of their drinking water. Since the start of the conflict, these pipelines have operated far below capacity, deliberately leaving areas of Gaza without water.

The entire population of Gaza is now facing severe and lasting physical and mental harm from malnutrition. For many children, survival will mean a lifetime of irreversible damage.

Humanitarian aid has also been intentionally obstructed through border closures, attacks on aid workers, and along distribution routes. Between February and March, Israel allowed less than a quarter of Gaza’s minimum needs for food to enter the territory.

Since May, the large majority of food aid allowed into Gaza by Israeli authorities has come from the US- and Israel-backed Gaza Humanitarian Foundation (GHF). The GHF's intentionally and dangerously designed distribution system relies on only three food distribution points – compared to the over 100 locations permitted under the previous UN-run aid system. All three points are located in dangerous, remote, and militarized evacuation zones: between May 27 and July 21, 2025, over 1,000 Gazans were killed while attempting to access food aid, with three-quarters of those deaths occurring near GHF’s distribution sites. The head of the United Nations Relief and Works Agency chief has called the GHF system a “death trap.”

Local food systems are collapsing as part of the systematic assault on Palestinian life. Mass dispossession and displacement are being accompanied by the calculated decimation of crucial food systems infrastructure – including farmland, wells, markets, and shops – undermining the foundations of food production and distribution. Israeli customs officials are throwing out fruits and vegetables with pits or seeds from humanitarian aid to prevent Palestinian's from growing food. Fishing has been rendered all but impossible through growing restrictions and military attacks on fishers, and landing and aquaculture sites. These violations also extend beyond the Gaza Strip: in July, Israeli occupation forces attacked the Union of Agricultural Work Committees (UAWC) Seed Bank in the West Bank, demolishing essential storage facilities and infrastructure for agricultural materials and inputs – a direct assault on Palestinian knowledge and heritage, food sovereignty, and efforts to preserve seeds and livelihoods.

These atrocities are also perpetuated by political and economic systems at both the national and international levels. The decisions of governments and corporations around the world – including complicity, material support, or inaction – directly impact Palestinian’s ability to access food and water, and live in dignity. For decades, many of these actors have directly and indirectly contributed to Israel’s illegal occupation, apartheid, and ongoing genocide in of Palestine. The UN Special Rapporteur on the situation of human rights in the Palestinian territories identifies 48 major corporate actors embedded in and profiting from “an economy of genocide”, benefiting from land and resource dispossession of Palestinians. In particular, agribusinesses, retailers, and logistics companies are pushing the products grown from Israeli occupation onto global markets, often through misleading or unclear labeling and little to no regulatory oversight.

Global trade with and investment flows into Israel have also continued uninterrupted. Many governments and institutions are actively investing in Israel, regardless of their political statements on Israeli violence, with the EU acting as Israel’s largest investor, followed by the US. A 2024 report revealed the involvement of over 800 European financial institutions (e.g., banks, pension funds, asset management firms) in Israel's occupation of Palestine.

IPES-Food stands in solidarity and support for the Palestinian people. Justice requires their right to self-determination, their right to food and food sovereignty, and their right to remain in on and return to their territories, and use the land, rivers and coast to build food sovereignty. We reiterate our urgent call for an end to the use of food and water as a weapon of war in Gaza, and in other regions including Sudan, South Sudan, and Yemen.

We call for an immediate ceasefire, an end to Israel’s assault on Palestinian territories, and restoration, reparation, and accountability for the decades-long occupation, oppression, and crimes committed against the people, land, waters and seeds of Palestine. This requires preserving and upholding international law, and guaranteeing that governments and corporations are held responsible for their complicity in this crisis, as already called for by the UN Special Rapporteur on the Right to Food and UN Special Rapporteur on the Palestinian territories. This includes states’ obligation to support and take concrete measures to repair and restore for the grave harm and violations caused.

We remind states, and public and private institutions of their legal and moral obligation to boycott, divest, and impose sanctions on the State of Israel, as is legally mandated by the 1948 Genocide Convention. Under international law, states have a binding obligation to actively prevent and condemn genocide, and to ensure they are never complicit in these crimes. The intentional denial of food and water in Gaza also represents a violation of the international human right to food and the right of self-determination, breaching humanitarian law, which states have binding obligations to uphold.

We condemn the Gaza Humanitarian Foundation experiment, and its instrumentalization of humanitarian aid delivery. We demand the immediate reinstatement and strengthening of UNRWA as the central and legitimate means through which international humanitarian assistance is delivered to Palestinians, alongside a more robust UN humanitarian system free from conditionality and political manipulation.

We call for broader participation of governments in the Hague Group and meeting the commitments being made to dismantle the ongoing systems of oppression and destruction of Palestinian lands and people. We commend the creation of the Hague Group in January 2025 and its engagement in coordinating legal and diplomatic measures to uphold principles of international law and put an end to the ongoing genocide.

For more background on the long history of the Israeli government imposing food apartheid on Gaza and the West Bank, please check out this episode of The Checkout podcast. Further resources and info here and here.

3. Why Sprouts Is Winning. For Now.

1. Sprouts Q2 Highlights: Another Big quarter.

Natural/Specialty grocer Sprouts is on fire. Revenue was up 17.3%. Comp sales up 10.2%. Adjusted EBITDA margin, 9.8% and net income was @6% of sales. Not a “razor thin” profit margin like the industry usually produces, but likely too high to be sustainable, reminiscent of pre-Amazon Whole Foods, very dependent on what suppliers are willing to subsidize and what Sprouts can grind out of employee productivity or gleaning margin off of customer price hikes. Perfect to appease Wall Street’s quarterly guillotine.

Their gross margin performance was primarily due to “leveraging inventory and category management improvements, as well as leverage from strong sales performance”, meaning that they got more trade spend out of suppliers, and this “inside revenue”, such as the 6% EDLC (everyday discount) scanback they requested of key center store suppliers last year compounded as topline sales continued to increase on the momentum of shoppers’ interest in healthy living.

This is “inside revenue” because the discount is not passed on to customers. Sprouts just pockets it. Kinda funny how analysts, trade and mainstream media, and even academia don’t usually mention this, nor is it mentioned in earnings or annual reports. But it is material and quite similar to how Whole Foods and wholesaler UNFI operates. The hottest grocery trend: pocketing supplier discounts to pad margins to juice investor returns. Robin Hood In Reverse.

Customer traffic was strong and accounted for the majority of the comparable store (comp) sales increase. But this means price inflation likely accounted for a significant share of growth, possibly 4-5%, meaning in store prices went up higher than overall inflation.

So, some quick math. If Sprouts net income was 6%, @4-5% of it was price inflation and the other 1-2% can easily be accounted for in the EDLC scanback “inside revenue”. Yes, this is a highly reductionist analysis that ignores much of what they do well as a retailer- see below- and yet, is it wrong? Grocery after all, is still a racket.

If so, this is a brilliant, short term, highly extractive strategy. Wall Street will love it. While it lasts.

More highlights: The biggest beneficiary of the UNFI cyberattack was Sprouts, who is primarily supplied by UNFI rival KeHe. Sprouts stores saw additional traffic when shoppers couldn't find things elsewhere. Sprouts E-comm sales grew 27%, representing around 15% of total sales for the quarter. Sprouts store brands contributed 24% to total Q2 sales, a huge growth engine over the past few years as they expanded both market share and category share in much of the store. Sprouts plans to release over 350 new private label products this year alone, which will put significant pressure on both incumbent natural specialty brands as well as make the chances of success for emerging brands that much more difficult. And Sprouts Rewards loyalty program launched in Arizona this month, the results showing that loyalty members are shopping more frequently and spending more.

Sprouts’ success is a strong indicator of the mainstreaming of health and wellness, especially in organic produce. They continue to expand SKU count in organic produce and trending “BFY” categories such as seed oil free and high protein, now offering more than 3,700 high protein products, with 450 new items set to be released this year. Things are looking up for Sprouts, no doubt.

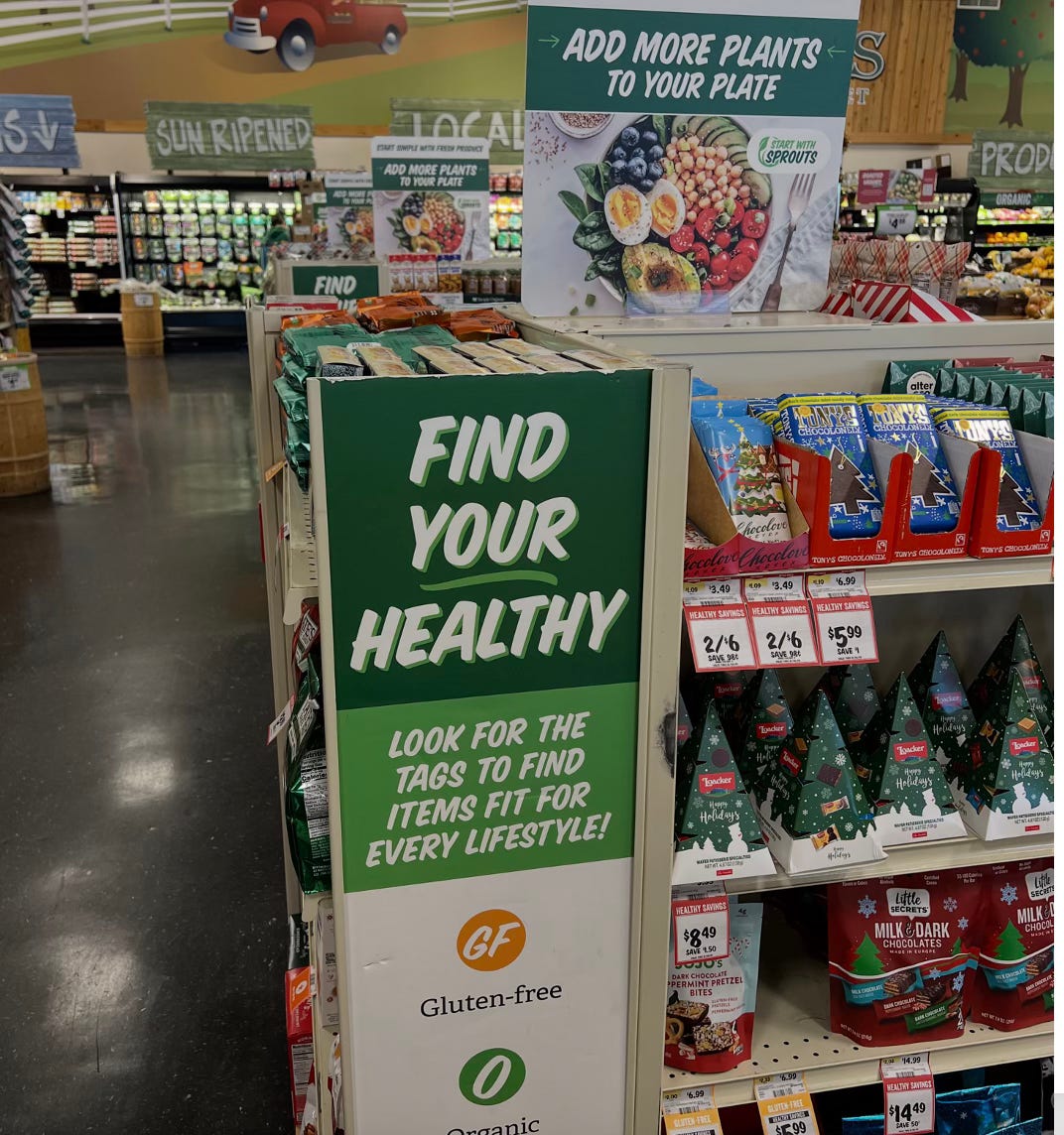

2. Sprouts: What’s Dope and What’s Nope?

Dope:

>Locations.

Sprouts has many great locations in working class and middle income areas, and a vibe that is less highfalutin, pandering and elitist than Whole Foods or Central Market. Their stores can really go anywhere and compete up and down market, whether with Fresh Market or most Kroger or Albertsons banners. They are a big threat to natural and organic indies and cooperatives, and are positioned similarly to Fresh Thyme, which has a much more limited market reach in the upper Midwest. The biggest external threats to Sprouts are the regional specialty chains that are priced more competitively while also playing heavily in natural/organic and “BFY” products, particularly HEB, Wegmans, Hy-Vee, Publix and Shoprite. But these threats are not existential and Sprouts can likely coexist alongside them.

>Open format layout.

The layout is wide open. When you walk into the store you can see straight across it. The shelves are low rise and not cavernous. The store is built inside out of the normal grocery geography. Sprouts leads with bulk and deli, including scoop bins and packaged products, testament to their retail legacy descended from Sun Harvest and Henry’s. Packaged grocery, dairy and frozen are in the rear on one side and on the other side is fresh produce, meat and poultry, including a full service case and self-serve. They have a modest HABA section in the middle of the store, alongside new item kiosks featuring trendy and innovative products, including locally-made brands. The stores are modest sized, easy to shop and navigate and don’t require much time to get in and out.

>Bulk hulk.

Sprouts continues to be a leader in bulk foods, especially since the Covid-19 pandemic when Whole Foods and many co-ops pulled back on bulk foods merchandising, especially in snacks and ready to eat products. Sprouts has a comprehensive bulk bin assortment, including culinary items such as rice, beans and grains, many types of nuts and dried fruits, and a broad selection of not-exactly-healthy candies, chocolates and other treats. The prices are not always cheap, because bulk foods require higher in-store labor costs for stocking, rotation and cleaning than packaged foods. And the quality and sourcing standards can vary. But there is no other national chain that puts as much store space, labor and inventory investment into bulk foods, or puts it front and center. It’s a cool move.

>Private Label.

Sprouts continues to revise, update and expand its store brands/private label selection. In previous years, when their store count was lower and they did not have the product volumes to support a broad own-brand strategy, Sprouts’ mix was more scattershot. For high volume commodity items, they used their own label. For specialized categories or more premium product segments, they used a range of in-store control brands that customers did not always connect back to the store brand. And they utilized wholesaler brands from their primary distributor KeHe to cover many packaged food lines. These days, they are expanding their own brand across the store, with hundreds of annual new launches, they are using private label in more premium categories such as nutrition, supplements and body care, and they are playing with creative and colorful packaging designs and labeling schemes to draw customer attention and reel in younger customers who have a different set of design and aesthetic preferences than older shoppers.

>Accessible health and wellness.

Not everything Sprouts sells is healthy. Ha, no way. They don’t really have very high ingredient standards. They sell some questionable stuff, especially in bulk. The stores are a bit grungy and don’t sparkle or smell like floor cleaner, essential oils or oat bran. But they lean much more heavily into organic and natural foods, plant-based products and wellness trends than most supermarkets. Their marking isn’t preachy or sanctimonious and shopping there isn’t a social signifier or a status symbol. The parking lots are a mix of sedans, hybrids and smaller SUVs and the occasional minivan, not as much the Beemer and Tahoe crowd. They have many locations in more middle income and out of the way suburbs and mid-sized cities, as well as the usual college towns, bustling suburbs and sunbelt cities. They go to market as an every-person’s destination for healthier living. It is working, for now.

>New item kiosks.

Sprouts, more than any other national chain, has become the destination for innovative consumer packaged goods and hot product trends. It is weird to even write that, as it was not the case for many years. In the past, Whole Foods Market and regional grocers like Wegman’s and Fairway dominated new item innovation. These days, as Whole Foods prefers to let other stores take on the risk of new product introductions and leans more into leveraging syndicated data to guide it’s “fast follower” category strategies, Sprouts has seized the opportunity with an aggressive and very visible new product merchandising and marketing vehicle, even waiving slotting fees for participating brands. In stores, the kiosks rotate a limited selection of new stuff every couple of months, with successful products getting slotted into mainline sets in the store. It is not an easy process for brands. The attrition and failure rate for new grocery brands is very high and only a select chosen few make it through the gauntlet of challenges, from competing with Sprouts’ own private label and well-placed incumbent national brands, to navigating wholesaler fees and inventory management and cost pressures in supply chains.

>Promotions.

Every endcap or display is a BOGO, a buy one/get one fully funded by suppliers. That seems to be the baseline for offshelf promotions at Sprouts. It is pretty compelling, with over a dozen endcaps, frozen bunkers, cooler, casestacks and other displays trumpeting their BOGO signage. Sprouts has always been an aggressive high-low retailer, with above market everyday prices balanced out by extensive weekly promotional markdowns funded by suppliers.

Sprouts is not a cheap partner for suppliers. They charge promotional placement fees, require suppliers to fund the majority of the markdowns through off invoice, charge-back or scanback discounts and encourage serious, long term suppliers to drop a 6% everyday discount (EDLC) as a sign of good faith partnership in the future of their business. This 6% “kickback” is a response to Whole Foods 3% merchandising fee on top of UNFI’s 2.5% data access fee, so Sprouts one-upped the 5.5% of their rivals. “Inside revenue” for the win.

And this is all on top of the 15-20% of annual sales that center store suppliers spend with Sprouts on promotions. It is a very expensive business and filters out undercapitalized brands that aren’t willing to pay to play. But suppliers typically expect strong execution and retail follow through on their discounts, they mostly get good return on investment and promotional sales lift and velocities, and Sprouts retains and attracts customers that keep them coming back for more, ensuring that most suppliers are willing to keep investing in this promotional strategy that is driving comparative sales growth, margin dollars and consumption volumes, as long as the company keeps growing.

>Thorough CPG selection.

Outside of Whole Foods Market, Fresh Thyme and a handful of larger co-ops like PCC, The Wedge and Park Slope, there are not many grocers that carry as deep and broad mix of natural, organic and minimally processed, “better for you” grocery products. Sprouts comes out of a similar retail tradition as Whole Foods, in that it uses medium to large scale retail formats, industry-leading cost plus wholesaler agreements and expansive supplier partnerships to make sure it has what those folks who are trying to eat healthier on a budget, just had kids, are being more careful as they get older, don’t like the upscale, elitist vibes at Whole Foods or crunchier natural food stores, or don’t feel like playing “where’s Waldo” at a massive Meijer, Kroger, HyVee or Albertsons to locate the core mix of natural and organic products that they want. Sprouts carries all the usual suspects, the Bob’s, the Amy’s, the Annie’s, the Dave’s Killer Breads, plus plenty of Impossible Burgers and meat analogues. They sell sustainable seafood and cage-free and antibiotic free meat and poultry. It’s not the highest standards, highest quality, strictest baselines or best in class anything, but they position it as accessible enough so that they can open these stores in those locations that may not meet all the demographic criteria that their upmarket competitors require.

>Improved produce.

Their produce is now 50/50 organic and conventional, almost on par with Whole Foods (@55% organic) but nowhere near the 100% organic at Natural Grocers or 98% at PCC. The quality is significantly better than in previous years, and is at least comparable to most mainstream supermarkets in price, quality and freshness, when store conditions permit, that is.

Nope:

Sprouts has many areas of vulnerability. Here’s the top few.

>Gross old stores.

Their biggest internal challenges are the overinvestment in new store development at the expense of ignoring aging incumbent locations, many of which degrade quickly due to the focus on bulk and perishable inventories, along with high staff turnover and a non-union workforce. Older locations tend to be grungy, smell moldy and rotten and have fixtures, coolers and freezers that need to be updated or replaced. Not pleasant. The new stores are beautiful, but they too will degrade quickly unless invested in.

>Not very strict sourcing or ingredient standard baselines.

They market higher attribute products but also sell plenty of conventional items in deli and produce. Their egg, meat and poultry standards are very much a lowest common denominator of humanely raised, cage free, free range, and industrial scale organic, with some dabbling in pasture-raised, biodynamic and regenerative. They do not have much of a focus on fair trade or socially responsible sourcing in supply chains. They are not on par with Natural Grocers, who has much stricter baseline standards, but overlap significantly with Whole Foods, who has watered down their meat and poultry assortment and animal products supplier mix since the Amazon takeover. They still sell significantly less of the mass market, chemical intensive, factory farmed meat and poultry than larger supermarket rivals.

>Bulk junk.

They sell lots of snacks, candy and junk food in bulk, along with a smattering of healthier options with varying quality. So let’s be real what the draw is to bulk. It’s the candy. The sweets. The snacks. Ultraprocessed foods. The craveable stuff. Lots of it. They removed artificial colors to please the MAHA crowd, but competitors like WFM never allowed this in the first place. The quality of bulk nuts and dried fruit is also not consistent, due to both sourcing specs as well as bin rotation and cleanings.

>The deli and prepared foods selection is subpar and is not much of a draw.

It is so unremarkable that I typically go right past it on the way to produce. The Applegate deli meats were overpriced last I checked. The cheese selection is mid.

>High supplier fees and high brand turnover.

This is including the 6% everyday scan, high slotting fees, very high promotional and marketing fees and markdown expenses, including required funding of buy one/get ones on off shelf displays. As long as they keep growing, suppliers will keep throwing money at them for their market access. Once they slow down, expect more pushback and public denunciations of their trade practices, as well as a growing group of brands who won’t do business with them.

>Overpriced for the quality.

While there are good promotional deals and store brand items across the store, prices can be pretty ridiculous on many center store products and perimeter. Their sales numbers indicate price increases are still driving a big chunk of growth, and that is only as sustainable as what customers will tolerate. They are betting that their new loyalty program along with store openings, emphasis of mass market organic products, continued private label growth, E-Comm growth and supplier-funded promotional activities will keep those customer counts, consumption volumes and basket numbers on the upswing. It is a big bet.

>Staffing at Sprouts is a very conventional, top-down model.

They are union-free and similar to Whole Foods in their approach to morale building and employee socialization. The stores tend to have high turnover of entry level staff, and since they have full service meat, poultry and deli cases, do require significant staffing levels. Stock clerks in center store are required to make certain case stocking requirements on every shift, which can be challenging during the day when they are also helping customers or navigating around shopping carts. The checkout counters are partially staffed, but the stores are increasingly using self-checkout kiosks, staffed by one or two clerks or supervisors.

Sprouts is not a top tier employer. They are not a Wegmans or Publix. The pay is modest, the work is hard and there are few long term perks other than hoping the company continues to grow, open new stores and create new opportunities for upward mobility. Their staff will likely push to unionize in the future, especially as competitive pricing pressures along with costs of living continue to increase and once the store opening pipeline slows down. And once those comps slow down and EBIDTA margins cool off, lowering investor returns, Wall Street will call for blood. This is inevitable for publicly traded companies and will make the employee situation more dire. The first Sprouts union is only a matter of time.

peace.

(Disclaimer: Perspectives do not reflect those of our sponsors.)

Yes

Thank you

This is seriously insightful! While running Primary Beans, we almost had a shot at their innovation table, but they went with an ROC brand instead. Word is, they’re following in Whole Foods’ foodsteps.