Grocery Update Volume 2, #7: When UNFI Sneezes.

Also: How One Startup is Rewriting the Rules of Food Distribution.

Discontents: 1. When UNFI Sneezes. 2. How One Startup is Rewriting the Rules of Food Distribution.

1. When UNFI Sneezes.

Originally Published in Forbes.com. Now free and unpaywalled for my friends!

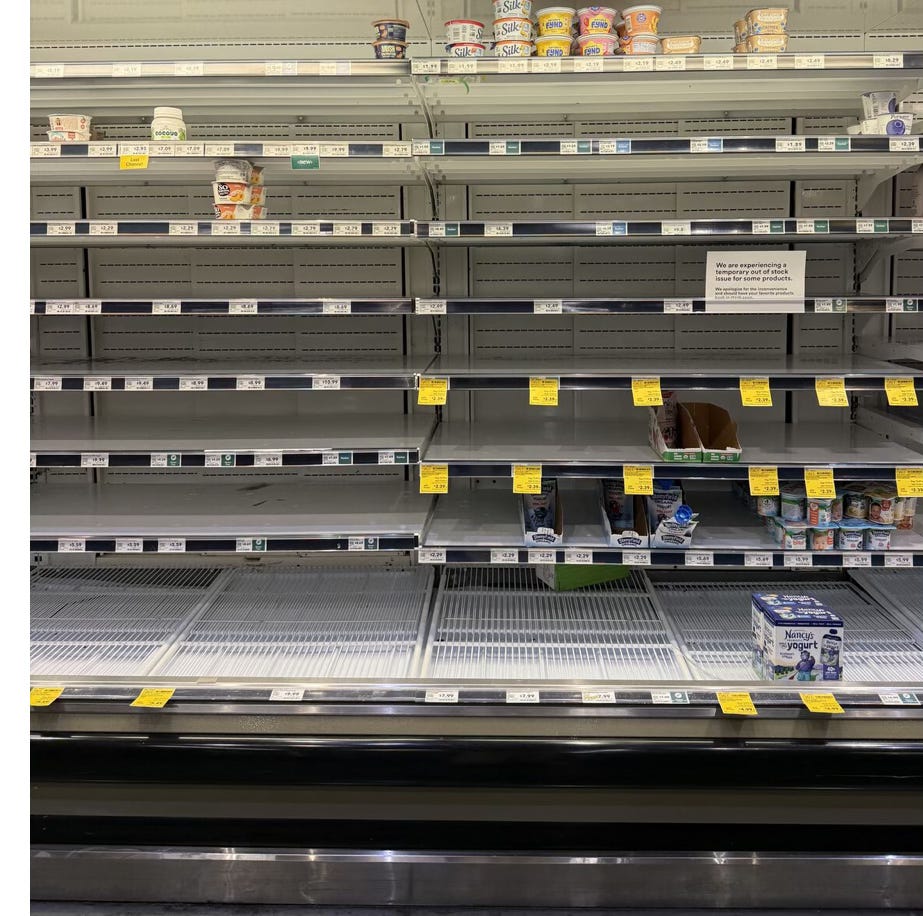

A cyberattack on June 5 crippled United Natural Foods (UNFI), a $30 billion grocery wholesaler and Whole Foods Market’s largest supplier.

UNFI also services more than 15,000 other supermarkets, cooperatives, health food stores and chain stores, and the company not yet sure when its ordering and replenishment systems will be able to fully supply its retail customers. Grocers have scrambled to access products from other wholesalers, putting pressure on supply chains throughout the industry.

While the cyberattack earned headlines for how it affected shoppers and store operations, the disruption also highlights the role of wholesalers in ensuring a functional U.S. food industry: When a wholesaler like UNFI sneezes, the grocery industry catches a cold.

Wholesalers like UNFI are the middlemen between suppliers and retailers in the packaged food industry.

Wholesalers are the vital connection between producers, manufacturers and retailers, and they command significant market access while working hand-in-glove with grocers on a daily basis. Though many retailers still do some of their own wholesale distribution, third parties like UNFI are essential to feeding many Americans.

Wholesalers handle millions of cases of product per day. They are large, complex, fast-paced work environments. They have very thin margins. UNFI gross margins typically hovers around 13.5%, a fraction of what retailers and manufacturers run on.

Besides UNFI, major wholesalers include $23 billion C&S, which supplies thousands of independent and chain-store supermarkets on the East coast of the U.S., and $50 billion McLane, wholly owned by Berkshire Hathaway and a major supplier to Walmart and Wawa. Others include Spartan Nash, partially owned by Amazon, and UNFI rival KeHe, an employee owned behemoth that services Sprouts, HEB, and thousands of independent natural foods and specialty food stores.

These wholesalers supply more than $300 billion a year in retail value, yet they are mostly invisible to consumers.

Wholesalers like UNFI and KeHe typically have primary relationships with grocers like Whole Foods and Sprouts, in that they distribute the lion’s share of their center store, beverage, dairy and frozen packaged food products. Grocers sometimes also use direct service snack and beverage operators like Frito-Lay, Pepsi, Snyder’s, Rainforest, and Dora’s Natural, or family owned specialty distributors like Chex Foods, as well as new item innovation focused start-ups like Pod Foods to diversify their supplier base. But the vast rows of empty shelves at Whole Foods and other stores illustrate the reach that primary wholesalers like UNFI have with their retail partners.

These wholesaler-retailer relationships are mutually dependent.

The retailers typically dictate what the wholesaler sells to them, based on their contractual obligations, their category management strategies, new product launches, private label programs and overall assortment blend by store, region and enterprise — all of which is usually specific to each wholesale warehouse location. The wholesaler in turn controls much of the market access for the thousands of brands and suppliers approved by retail buyers to sell into their stores.

In exchange for a low cost-plus markup, the retailer requires most of its suppliers to go through the wholesaler and drive large sales volumes, therefore justifying the low markup. The wholesaler typically guarantees product placement, inventory prioritization and better delivery schedules for its primary customers, especially during weather-related events or other disruptions. This relationship consolidates product distribution, creating a monopoly on supplying products into the grocer’s packaged food and beverage departments.

Wholesalers also tend to manage day to day relationships with suppliers on a more hands-on basis than grocers. When retailers approve placement of a product line in their stores, brands see it as a triumph that they got into the grocer. But this is really just the beginning. They must now keep the grocer happy and fulfill their promotional and inventory commitments and achieve sales and velocity hurdles to stay on shelf. They must also stay on the good side of their wholesale buyers.

The wholesaler needs to make a profit and has its own margin model, marketing programs, fees and assorted expenses that suppliers must cover from its gross margin and trade and marketing spends.

The core function of wholesalers, to distribute products into retailers, does not always pay their bills.

The markups wholesalers charge retailers are typically well below their cost of doing business. Retailers are under enormous pressure to compete with Walmart, discounters and dollar stores that are growing in market share and siphoning customers away. UNFI’s gross margin is usually in the 13-14% range. Their contractual markup to their largest customer, Whole Foods, is in the 6-7% range and even lower for Whole Foods’ store brand products. On the surface, this means UNFI is losing 6-7 points for every case of product it sends to Whole Foods.

UNFI must cover this spread in one of two ways in order to stay operational and earn a profit to keep shareholders happy. One way is by charging disproportionately higher markups to smaller independent retailers who are not part of an advantageous agreement that would bring their markups down. Such one-off independent stores sometimes pay 20-30% markups on the same items that a cost-plus retailer with larger scale pays 6-10% for. It behooves independents to join together and negotiate cooperative cost-plus agreements with wholesalers. Otherwise, it could mean that the retail prices at chain stores such as Kroger or Walmart could be lower than the wholesale cost that an independent grocer is paying, even before they add on their own retail markups.

The other way that wholesalers cover the cost-plus gaps is through inside margin from suppliers.

Such revenue streams include strict payment terms, such as a 60 day non-payment window when a product line is launched into retailers, as well as free fills and slotting fees, and various promotional discount models that suppliers must fund, such as MCBs (manufacturer charge backs), Off-Invoice discounts, as well as forward buys and bridge buys, where inventory is bought during discount periods and held to sell at regular prices after discounts periods are over. And then there is a range of obscure, confusing and frustrating accounting and payment practices to suppliers, such as invoice deductions, upcharges and billbacks for unsold, lost or damaged products, or outsourced labor fees for moving products around or between warehouses, called lumper fees. These are all major inside revenue streams for wholesalers that cover the spread between cost-plus markups and their gross margins, and are not discussed on earnings calls or CNBC segments.

The MCB is one of the industry’s most discussed and unpopular open secrets.

MCBs are a discount structure taken off the inbound cost of the product once it hits the wholesaler’s dock. Unlike off-invoice (OI) discounts, which transparently flow from supplier to wholesaler and on to the retailer and the end consumer, the MCB is billed back to the supplier at an additional retail markup, called the full-wholesale price. On paper, this inflates the cost of the supplier’s product, thereby also inflating the value of the discount that the wholesaler can grab and the supplier must pay, essentially applying a markup on the markdown.

A supplier taking 20% off their list cost could end up being billed back for 35-40% of the cost of their product. Many retailers, such as Whole Foods and Sprouts, have gotten wise to MCB practices. But instead of disallowing such markups on supplier markdowns, they just contractually require wholesalers to rebate a portion of their cut back to the retailers, called a true-up.

Most items on sale at grocers that pull from UNFI or KeHe are funded by MCB monies. But many suppliers actually prefer the MCB discounts because OI discounts can be worse.

Wholesalers and retailers can require suppliers to do regular OI-funded promotions, because they discount the value of the inventory sent to retailers and the accounting is easier. But OI discounts can mean that wholesalers can forward buy large amounts of product on discount just as a sale period is ending, allowing them to sell much of it at a regular price at much higher margins. Or the wholesaler can bridge buy between promotional periods, loading up on enough inventory at the end of one sale period to carry through until the next sales period a few weeks or months down the line, so they never have to buy products at regular cost from suppliers, eating into supplier margins, and all the while selling the products to retailers at a higher margin and not reflecting the discounted inventory to their retail customers or end consumers in the form of in-store sale prices.

When a supplier is covering the wholesaler’s bridge buy or forward buy, on top of funding aggressive promotions, such as the BOGO (buy one, get one) offers heavily marketed at Sprouts, it can be devastating to their business. And suppliers will see little to no return on investment on these trade dollars, unless they count not running afoul of their wholesalers as a good use of funds. Fear is also currency.

And eventually, this fear translates into higher costs for consumers, as suppliers can only squeeze so much out of their margins before they pass those costs on down the line to consumers, or they can go out of business. In the 19th century, Joseph Schumpeter heralded capitalism as creative destruction. He had no idea how creative that destruction could get.

There are plenty of other common wholesaler practices that suppliers, especially independent and family-owned emerging brands, deal with regularly: being charged the same fees twice; being paid late and receiving early payment deductions in spite of this; systematically being withheld payment; paying warehouse activation fees or listing fees/discounts that are not contractually required; getting billed for monthly specials and flyer programs they did not agree to pay for; erroneous deductions with no backups to review, sometimes for thousands of dollars at a time; vague and confusing deduction and billback documentation for shrink or damages; being billed for out of temp product the wholesaler sent to a retailer, especially when the retailers refuse product and send it back to the wholesaler; being billed for free fills and slotting even when retailers have waived such fees; and paying for a highly essential cottage industry of forensic accountants who specialize in billback and deduction audits, dispute resolution and chasing refunds, some of whom are even familial relations to former executives at the very same wholesalers.

Such practices have become more commonplace as the wholesaler marketplace has further consolidated into fewer and larger enterprises, such as UNFI’s acquisition of SuperValu, which in turn was encouraged by investors spooked by Amazon buying up UNFI’s largest customer, Whole Foods. Scale begets scale.

Suppliers have little say in these matters, except for the occasional eruption of bad PR that is quickly quelled by wholesalers’ supplier relations staff. Retailers are contractually obligated to push suppliers into their primary wholesalers in order to reap the rewards of cost-plus agreements that shave 5-10% in savings on wholesale costs. This savings is material to their pricing strategy, customer retention and profitability. And by controlling market access to select, high profile retailers, wholesalers can make the rules and charge brands whatever this constricted market will bear. And it bears a lot.

Grocery retailers, fending off Walmart and Aldi on pricing, are ultimately responsible for how the wholesale sector functions.

There are few alternatives that can offer the broad range of goods at the low costs retailers are demanding to stay price competitive, especially as climate and trade war inflationary pressures are pushing up costs on key goods like coffee, cocoa, beef, European specialties, imported produce and packaging materials like steel and aluminum. Wholesalers like UNFI and KeHe have swallowed up many independent and cooperative competitors, and wholesale is now one of the most consolidated sectors of the food industry.

Some retailers, like HEB and Kroger, still self-distribute high volume packaged food products or have internalized wholesaler operations, such as Stop & Shop and Giant’s parent company Ahold-Delhaize.

Some lean on higher cost but more customer-service oriented wholesale operators that provide essential services, such as importation, product sourcing, private labeling, category management and in-store sales and merchandising support. And many retailers have banded together to form wholesale cooperatives that leverage collective scale to access products at competitive prices, such as the Greater Austin Merchants Association, Associated Wholesale Grocers or Twin Cities Co-op Partners. Wakefern, based in New Jersey, is the largest such cooperative, with nearly $20 billion in annual sales via hundreds of independent owner-operated stores such as Fairway and ShopRite. The New York City metro area is uniquely abundant with a number of independent and cooperative wholesale and retail operators.

But most U.S. metro areas are not so lucky, dominated not only by a handful of large grocery chains such as Walmart, Costco, Kroger and Albertsons, but also lacking in a diverse array of wholesalers that can supply the wide range of packaged foods that they sell every day. Scale begets scale; market concentration is a self-fulfilling prophecy.

And since market concentration also means pricing power, the costs of doing business are passed onto farmers, food workers, small businesses, emerging food brands and cash-strapped consumers, in the form of wage stagnation, higher food prices and draconian fees and invoice deductions. UNFI, after all, is still accountable to its institutional investors and shareholders, who want to see ongoing, profitable growth, no matter what. If grocery market consolidation had a mascot, it would be Robin Hood in reverse.

So while UNFI will hopefully recover quickly from the cyberattack and adopt better cyber security measures to ensure that millions of consumers have access to the food they eat everyday, the grocery industry lives with an ongoing structural dilemma. In an era of cybercrime, trade wars, climate change, pandemics and social upheaval, is a consolidated and opaque wholesale grocery sector the best way to stock grocery shelves and keep America fed? We won’t have long to wait for an answer. The next supply chain crisis is only a matter of time.

2. When “Yes” Isn’t Enough: How One Startup is Rewriting the Rules of Food Distribution.

By Torah Torres, Founder, Adventure CPG.

For small and emerging food brands, landing a buyer can feel like winning the lottery. A retail “yes” represents months—sometimes years—of hard work validated with a single word. But the celebration is often short-lived. Because that “yes” usually comes with a quiet clause: You must go through our preferred distributor.

For most brands, that’s where the problems begin.

Preferred distributors often require long-term contracts, impose steep fees, and operate within rigid systems that weren’t built for agility or fairness. Many brands are forced to give up margin, control, and even visibility into where—or if—their product ends up on shelves. It’s a system that rewards scale over substance and leaves smaller players with little room to grow.

Enter Adventure CPG.

Founded with a mission to level the playing field, Adventure CPG offers a radically different model—one built around membership, shared infrastructure, and aligned incentives. When a retailer agrees to carry a product, the brand simply uploads its information into Adventure CPG’s platform. From there, Adventure handles the distribution, negotiating directly with regional partners under its own contracts.

This isn’t about cutting distributors out—it’s about making their role more efficient and more profitable. Because Adventure operates its own warehouses, regional distributors no longer need to stock inventory. Instead, they fulfill pre-sold orders placed through the platform—removing the risk and overhead that typically burden these businesses. The result? Distributors earn more per delivery. Retailers get fresher product faster. Brands stay in control.

It’s a model in which, quite literally, everyone wins.

And in a post-UNFI world, that matters more than ever. When the country’s largest natural foods distributor experienced a massive cybersecurity breach in June, the fragility of the system became undeniable. Orders froze. Retailers panicked. Emerging brands were pushed aside to make room for bigger accounts. The ripple effects were a reminder that food distribution today is both over-centralized and under-protected.

Adventure CPG’s decentralized, tech-enabled infrastructure offers something that’s been missing from the industry: resilience. By distributing risk and power more evenly across brands, retailers, and delivery partners, it creates a system that works not just during good times—but when things go wrong.

It’s not a workaround. It’s a reset.

And for founders who’ve built their brands on integrity, purpose, and product quality, that “yes” from a buyer finally means what it should: a clear path forward.

peace.

Didnt realize how much UNFI engaged in predator like practices untill I read this. Maybe thats why they got attacked