Grocery Update # 25: The Case For Employee Owned Grocers.

Also: Cows Don't Milk Themselves. And A Potato Chip Throwdown.

Discontents: 1. Cows Don't Milk Themselves. 2. The Case For Employee Owned Grocers. 3. A Potato Chip Throwdown. 4. Tunes

1. The Cows Don’t Milk Themselves.

Most farms are too big just for farmers and their families to do all the work. They have to hire workers. They are turning to immigrant and undocumented workers to do this, mostly invisible work, on dairy farms. Migrant farmworkers tend to be among the most underpaid, exploited and vulnerable populations in the food system, subject to racial stereotypes, wage theft, substandard housing, sexual violence, harassment by law enforcement and even deportation by immigration authorities. But these essential workers are fighting back.

Migrant Justice is a Vermont-based, dairy farmworker-led organization working for justice and dignity in their communities. Their Milk with Dignity Program was inspired and influenced by the highly successful Coalition of Immokalee Workers (CIW) Fair Food Program. Known as worker-driven social responsibility programs (WSRs), they are designed and led by farmworkers and have been proven by a ten-year longitudinal study to be the among most effective framework for protecting human rights in supply chains, more so than fair trade or voluntary corporate responsibility programs.

WSRs are effective because they leverage consumer-facing campaigns while creating legally binding frameworks and enforcement mechanisms between the corporate buyers and the WSR certified farms. This framework connects the dots between consumer expectations of sustainability, while de-risking supply chains for retailers and investors. But most importantly, WSRs ensure fair pay for farmworkers and prevent forced labor, harassment and sexual violence on farms. Like trade unions and collective bargaining, WSRs give farmworkers a seat at the table and a big say in improving their quality of life. This shows in the numbers that Milk With Dignity has documented:

256 qualifying workers on 54 participating farms across 2 states

20% of Vermont’s total dairy production covered by the Program

$5.35 million invested in workers’ wages and bonuses and in improvements to labor and housing conditions

611 violations of the farmworker Code of Conduct resolved

212 farm audits, including 941 farmworker interviews, 315 management interviews, 268 worksite inspections, and 218 housing unit inspections

2,281 audit findings addressed through Corrective Action Plans agreed to by farmers

247 Program education sessions, with 1,291 worker and manager participants

Workers aren’t the only ones benefiting from Milk with Dignity. Farm owners even think “programs like Milk With Dignity are what Vermont agriculture needs to stay viable.”

However, the success of Milk With Dignity has created a two tiered milk supply in Vermont: workers covered by the program, and those that are not. Brands like Ben & Jerry’s have been leaders in working with Migrant Justice. But some retailers are not on board.

Kroger, the U.S.A.’s second largest grocery chain, and Hannaford, a New England division of international grocery conglomerate Ahold-Delhaize (who also owns Food Lion, Giant and Stop&Shop), have both refused to partner with worker-led organizations like CIW and Migrant Justice. Respectively, and not surprisingly, the produce and dairy supply chains of both grocers have been linked with forced labor and trafficking of migrant workers.

Hannaford in particular has an opportunity to ensure that their store-brand milk is produced without human rights violations. Their stores in Vermont source milk from farms all over the state. Hannaford’s internal social responsibility program has not done much to protect farmworkers, their “speak-up” phone line is ineffective.

Readers can support dairy workers' rights by calling on Hannaford to join the Milk with Dignity Program.

Ervin, a farmworker in Milk With Dignity, sums it up: “Farms need us. These companies need us. If there weren’t agriculture, there wouldn’t be food. We deserve a dignified living. That’s what everyone deserves.”

2. Redner’s And The Case For Employee Owned Grocers.

Redner’s is a family and employee owned grocery chain in eastern Pennsylvania with 66 or so locations. I had never heard of them until spending time in the Philadelphia area. Redner’s is based in Reading (pronounced Red-ing), a diverse, busy industrial hub nestled in the rolling Appalachian foothills, about halfway between Harrisburg and the endless Philly suburbs. Philly and eastern PA. have a pretty diverse grocery scene. Even though Acme (Albertsons), Giant (Ahold), Walmart and ShopRite own big market shares, Aldi and Lidl have established toeholds, and dollar stores are spreading everywhere, there are plenty of other high quality grocers, including Redner’s, Kimberton Whole Foods, Weaver’s Way and family owned behemoth Wegman’s.

I am enthusiastic about employee owned stores and try to visit them when passing through. Chains like Hyvee, Winco, Market Basket (or Maahhkit Basket as the Boston locals say), HEB, Brookshire Brothers and Florida’s favorite monopolist Publix have big employee ownership stakes. The data shows that employee ownership is an effective vehicle for working class folks to make a decent living, have a stable career and enjoy their work. Stock clerks, dairy buyers, cashiers, inventory specialists, receivers, truck drivers, meat cutters, all with real skin in the game, not just cogs in the apparatus.

Employee ownership, through ESOPs (employee stock ownership plans), employee owned trusts and my favorite model, worker cooperatives, have a compelling track record, with 33% higher median income, a 92% higher median household net wealth, and 53% more job stability. There are differences of course. ESOPs and EOTs tend to have more traditional, hierarchical management models, while worker cooperatives tend to be more horizontal, like Rainbow Grocery in San Fran. Unions can and do exist in such settings. But sometimes companies leverage employee ownership to keep unions out. Not cool. But employee ownership is still a viable, pragmatic alternative to corporate extraction and expendability. Unlike Walmart, Amazon or Target, employee ownership means that more blue collar employees get to enjoy the fruits of long term growth. Run it like you own it, because you actually do.

Employee ownership, like consumer cooperativism, doesn’t fit neatly into 19th century economic dogmas. Is employee ownership capitalism? Well, sort of. These businesses must generate a profit, but much of the capital is held in common by people doing the productive labor, and not only executives, asset managers or private equities. Or is employee ownership a form of socialism? Well, kind of. At least more so than the bureaucratic state capitalism in the Soviet Union, where workers’ wealth was extracted by the government, in place of big business. Employee-owned enterprises still need to function with appropriate gross margins, marketing and pricing strategies, promotions, everyday low price segments, a full retail assortment of grocery, produce, meat, bread, etc. But the wealth is spread a bit more equitably than say the Walton clan owning 46% of Walmart, or Dan McMillon or Rodney McMullen making 900 or so times the average Walmart or Kroger worker, respectively.

Employee ownership connects the dots between the conservative icon Ronald Reagan and the libertarian socialist Richard Wolffe, oddly enough. And employee ownership is anti-fragile, built to withstand our compounding crises. Maybe employee ownership is one big way to heal our fractured society.

The other thing I have frequently noticed about employee owned shops is the artisanship of merchandising. This is something they have in common with some of the best run union shops, like Fairway or some Kroger divisions, or best in class independents such as Kimberton Whole Foods or Good Earth Natural Foods. You can tell the employees give a shit. The stores sparkle. They are works of art, well faced, fronted, clean, fully stocked, accurately signed and priced. Or is that just my own confirmation bias? Maybe, I am not objective. I just call it like I see it.

Now Back To Redner’s.

The vibe is nicer than your average Safeway or Randall’s, but the prices seem more reasonable. Walking into the store, the lighting, fixtures and flooring are dark and subdued. Square fluorescent light fixtures in a checkerboard black ceiling. Black point of purchase racks and coolers. Very different than HEB or Food Lion, which always feel so bright, shouty and hyper (which works fine for them).

Up front, neatly displayed endcaps with vertical strip merchandising by sku and by color, Lucky Charms, Cinnamon Toast Crunch and Reese’s Puffs cereals, at 2/$7, with Halloween versions of each cleverly placed at eye level at $3.69 each. Sugar bombs for breakfast. A Pepsi rack with shelves of 2 liter bottles at 2/$6 flanking a branded Frito Lay rack with Ruffles, Lay’s, Tostitos, Doritos, Fritos and Munchies (party size, of course). Adjacent to a Coca-Cola power stack, dozens of cases of 12 oz. cans and bottles, buy 2 get 2 free, a high margin temptation for your thirst (and diabetes).

Redner’s merchandising is a bit tighter than your average Giant or Acme. Produce felt a little thin, though. The quality was fine, mostly conventional, plenty of in-season and local. A standard industrial produce assortment stacked and bundled neatly. They had a little organic section, a lot of Wild Harvest bagged and packaged items. Wild Harvest is a house brand of UNFI, and I noticed a lot of UNFI store brands around the store acting as a consistent value tier. Redner’s also had an old-school, store-within-a-store allergen friendly, natural, plant-based and organic packaged food section. That is a good way to keep up with Wegman’s. I love Wegman’s, but I find their sets overdone and way too big. Redner’s was pretty tight, with plenty of gluten free, grain free and organic snacks and treats.

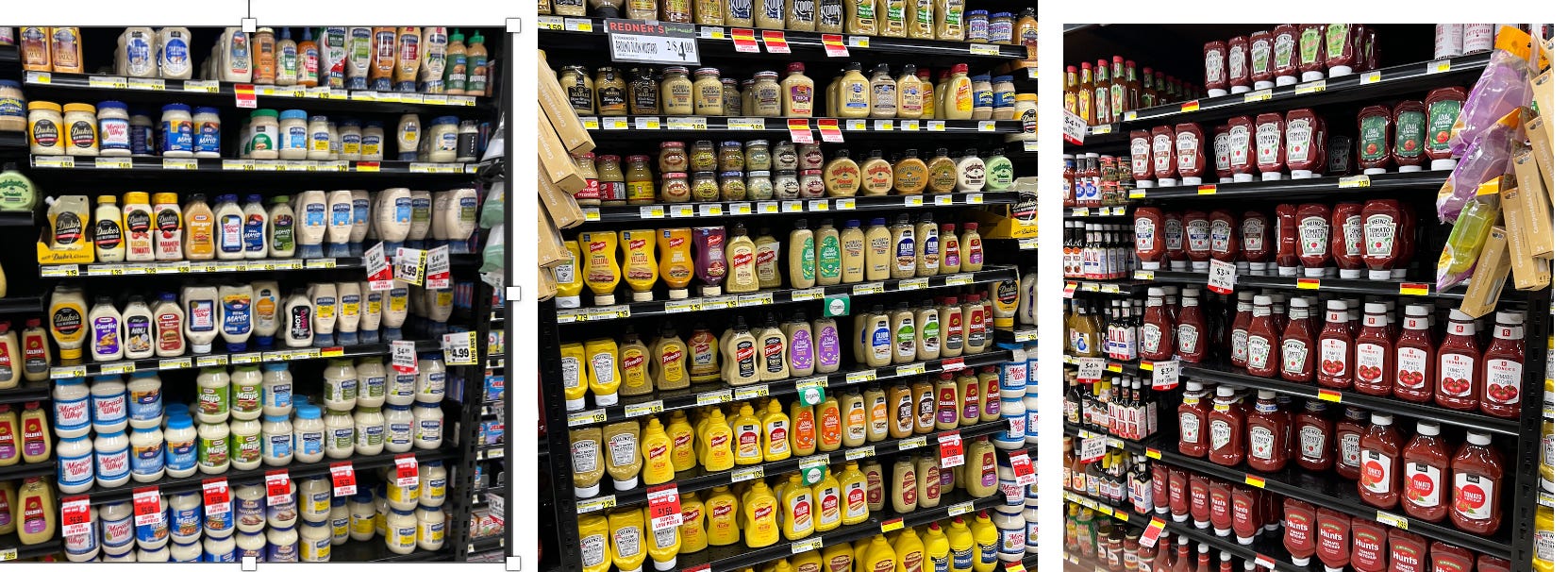

Redner’s had several aisles of ambient grocery. The shelving was a dark, sturdy, industrial racking setup, not your typical Lozier or Madix gondola. This gave the stores a more warehouse vibe, but they also framed the product sets in a really easy to shop method. Sure, there was brand blocking, but in sections like condiments, paper goods, canned tomatoes and vegetables, the racking carved out some of the neatest, most easily shoppable sets I have seen in the industry.

The racking also enabled lots of backstock to be piled high by set, so it could easily be restocked instead of being hidden and buried in the back room where it could go out of date or get damaged. I counted cases of backstock in a few sections and two things were quite obvious. One, the replenishment buyers were forward buying on promotion to juice their margins by selling at regular price after the discount period was over. This is standard grocery practice to stay profitable. I guessed they held under 20% of their inventory in such backstock, but I would also guess that the forward buying gave them another 4-5% of incremental center store gross margin padding. Two, this indicated that they weren’t beholden to “lean” production and “just in time” inventory systems, like so many publicly traded and private equity owned grocers trying to keep cash off their balance sheets in order to appease Harvard-educated finance spreadsheet jockeys. I know where I would shop before a big storm. Redner’s would have a decent supply of long code ambient products because that was part of their business model. No truck to shelf bullshit.

And the UNFI/Super Valu private label value brands were well stocked in center store. Lots of Essential Everyday pantry items alongside the usual suspects from Conagra, Kraft Heinz, General Mills, Nestle, Kellogg’s. Hunt’s, Ragu, Delmonte, Herdez, Lawry’s, Duke’s, Miracle Whip, French’s. Manwich. Lots of Manwich in the overstock too. Must have been a Manwich promotion. Who still eats so much Manwhich? And Velveeta vs. Hamburger Helper “meal kits”. Skippy, Jif, Peter Pan and Redner’s own brand of nut butters. Probably the most comprehensive Oreo section crammed into four feet, including a shelf of gluten free versions and a whole shelf of Oreo Thins. Oreo-e-o.

An extensive salty snacks aisle, well stocked with Pepsico/Frito Lay’s best and brightest, but also plenty of eastern PA’s local favorites, like Wise, Herr’s and Utz.

Frozen foods were likewise stocked with a comprehensive mix of value items and consumer brands. UNFI’s Wild Harvest, Woodstock and Essential Everyday in frozen fruits and vegetables, alongside Dole and Birdseye. Hungry Man (what is with all this gendering of ultraprocessed foods?) at 2/$8, Stauffer’s, Lean Cuisine, “Mega Bowls”, Banquet, Ore-Ida, Mrs. T’s (pierogies, no relation to B.A. Baracus), Tombstone pies at 2/$9.00. Doors upon doors of ice cream scrounds, Breyer’s, Turkey Hill, Blue Bunny.

Lots of milk, with three varieties of conventional and locally produced milk, including Clover Farms at $4.07 a gallon, Redner’s at $4.53 and Rosenberg’s at $4.93. Better milk prices than Walmart and nice price tiers! Several doors of competitively priced, packaged, processed cheese from Sargento, Borden, Crystal Springs, Essential Everyday, Cabot, Kraft and more, sliced, shredded in convenient, resealable plastic packaging destined for landfills. So much cheese, jeez.

And as a full service grocer, Redner’s also had a staffed meat and poultry case. At their scale, they were mostly stocking industrial, factory farmed chicken, beef and pork. Some great prices, like $2.69 boneless chicken breasts, alongside more premium, humanely raised, antibiotic and hormone free, grass fed and organic items, with signage calling out those attributes. And lots of sausages. So many sausages. Mostly pork, occasionally chicken or beef. Pennsylvanians like their meats.

This is mainstream, industrial food merchandising at its best.

Redner’s is a masterclass in modern grocery retail, showing that even in a highly consolidated sector with plenty of price, assortment, format overlap and competition, an employee owned chain can hold its own. Employee ownership for the win.

3. Potato Chip Smackdown.

Potato chips are a big subcategory, part of the even larger salty snacks category. Salty snacks is probably the most profitable aisle in grocery stores in terms of sheer dollars, and besides soft drinks, usually the largest in sales volume. In 2023, Americans bought 2.65 billion bags of potato chips, for an average retail price of $3.22, generating $8.5 billion in sales. Compared to 1.85 billion bags of tortilla chips and 2.3 billion boxes of crackers, potato chips are among the most popular shelf stable snacks. Potato chips have gone up 43% in price in the last 4 years and Americans are actually buying 3.5% fewer bags than in 2019.

They are also a heavily monopolized category, with Frito Lay owning upwards of 50% market share in many metro areas. Despite this, there is an enormous variety of potato chip brands, especially when you go to independent and locally owned grocers who have some bandwidth and flexibility in their merchandising. Indies may be taking Frito money for DSD (direct service delivery) stocking in stores, endcaps and other displays, but they are by no means beholden to the salty snack mafia.

I went to three locally owned grocers over the course of a couple weeks and counted dozens of brands of potato chips and upwards of a hundred varieties. Those Pennsylvanians really like their potato chips.

I am not a potato chip aficionado by any stretch.

I actually hadn’t eaten many of them in the past few years. Too inflammatory, you know? If I eat processed potatoes, I usually prefer some tater tots. With ketchup and hot sauce. Call me basic. But this potato chip project was too tempting. I have a limited budget these days but decided to splurge and sample some of the more interesting looking varieties.

I did not pick up any private label brands from Wegman’s or Trader Joe’s. I didn’t go to Giant or Aldi/Lidl either. I decided to do a mix of national brands, local items and natural channel specific items. I only bought salted varieties, no flavors and did a mix of regular and kettle style. Oddly enough, I could not find any organic potato chips, so I am sure I metabolized my fair share of organophospates, herbicides and fungicides for this article. That is the sacrifice I make for my readers! Big shout out to the grocery staff of Redner’s in Collegeville, Karn’s Quality Foods in Harrisburg and Kimberton Whole Foods in Reading for doing such a great job keeping their aisles well stocked with such a range of snacks. So here are my tasting notes and buyer’s eye for a brief sample of Pennsylvania’s plethora of potato chips.

Ratings are up to 5 stars.

Keough’s: Cool graphics, nice story (Irish potatoes, grown and processed on farm). Chips were unpeeled, which is cool, but tasted bland, flat, uninspiring. 2 stars.

Uglies: Really cool blue bag, eye catching and kitchy graphic. Chips had a deep potato flavor, nice variation on size and shapes, some were a little overcooked, not too salty but tasty. “Upcycled” too. 4 stars. Would buy again.

Siete: Frito Lay’s newest acquisition. No seed oils. Warm, bright graphic design. Nostalgic deli style crunch and freshness, yet still lighter and crispier bite than most of the other kettle style chips. Fresh potato flavor and nice salt content. 4 stars. Would buy again except for it now being a Pepsico brand. Sad.

Cape Cod: The brand standard of kettle cooked chips, now owned by Snyder’s/Campbelll’s. Still an iconic package. The chips were perfect golden brown, both crispy and crunchy with good potato flavor and perfect saltiness. 5 stars, best of the batch. Would buy again.

Kettle Chips: Also owned by Snyder’s/Campbelll’s. The Starbucks of chips: overcooked, overmarketed, oversku’d. Overrated. Too bland and boring. 2 stars.

Boulder: Bland, flavorless with a mild crunch. As for the chips, why bother? 1 star.

Carolina Kettle: Never heard of this brand before. Homey, kitchy label, very un-corporate. Chips were light and thin, but very bland, pale and fragile. Meh. 2 stars.

Wise: I grew up on these. No wonder I hated food. Chips were weak and flaky, bland with a rancid oil vibe and kind of stale. Bodega chips. No real flavor. Sad chips. 1 star.

Lay’s: The category leader. Easily the thinnest, saltiest tasting. Decent flavor, all crisp, no crunch. I definitely see why they are so dominant and are the “NBE” or national brand equivalent for rival brands and private labels. 3 stars.

Utz: A local favorite. Chips were pale, like a cheap Lay’s knockoff. They had a slightly bitter finish, but were otherwise bland and boring. Another “why bother”? 1 star.

Dieffenbach’s: Quaint, old school graphics reminded me of the time when men were men and ate Manwich. Chips were thin cut, but had a strangely heavy taste that filled me with sadness. 2 stars.

Martin’s: Another local brand with old school graphic design. Definitely a Lay’s clone in cut, finish and color. Slightly burnt taste but fresh and light. Surprisingly ok. 3 stars.

Goodes: Another local brand. Regretted eating these. Pale, rancid, stale and weird off notes, almost gamey like lard or tallow fried. Why, god, why. 1 star.

So overall, big winner by a longshot was Cape Cod, with Uglies a distant second. Siete, honorable mention.

4. Tunes.

Another great song about working, from the classic British punk band Cock Sparrer. Somewhere stylistically between glam and Oi!. Nothing like making some cash off the books!

peace.

Ohh, wish you'd come to visit us at Radish & Rye while you were in Harrisburg!